Cash Balance Plans

Cut Your Tax Bill by Six Figures & Super-Fund Your Retirement

Part of Miser Wealth Partners — Integrated Tax, Legal & Investment Services.

For business owners and high-income professionals who want to turn their biggest expense into their most powerful asset.

No obligation • Complete confidentiality • Free consultation

On this page, you will learn:

- ✓What a Cash Balance Plan is and how it differs from a 401(k) or SEP IRA.

- ✓How to use a Cash Balance Plan to create six-figure tax deductions and significantly reduce your taxable income.

- ✓The ideal candidate profile for this powerful retirement savings strategy, including income levels and business structures (S-Corp, C-Corp, Partnership).

- ✓A real-world case study showing how a business owner saved $92,000 in taxes instantly.

- ✓The steps to implement a tax-deductible retirement plan before your tax deadline.

Why the Tax Code Has More Rules for Higher Earners

If you've built a thriving business or command a high income, you know that taxes are a significant cost. What's less obvious is how much more complex the tax code becomes as your income climbs — entirely new layers of rules, thresholds, and deductions come into play that simply don't exist at lower income levels.

It's not just one tax — it's layers of rules that come into play when you earn more, sell an asset, or tap your retirement money. This creates a “Blind Spot Tax” — a silent, compounding cost paid by smart, successful people who may not be aware of the full playbook of legal tax reduction strategies available to them.

Without a deliberate strategy to navigate these rules, you could keep paying more than you need to — year after year.

How a Cash Balance Plan Turns Your Biggest Liability into Your Greatest Asset

What if you could legally redirect six figures of your tax bill back into your own retirement account? That's the power of a Cash Balance Plan.

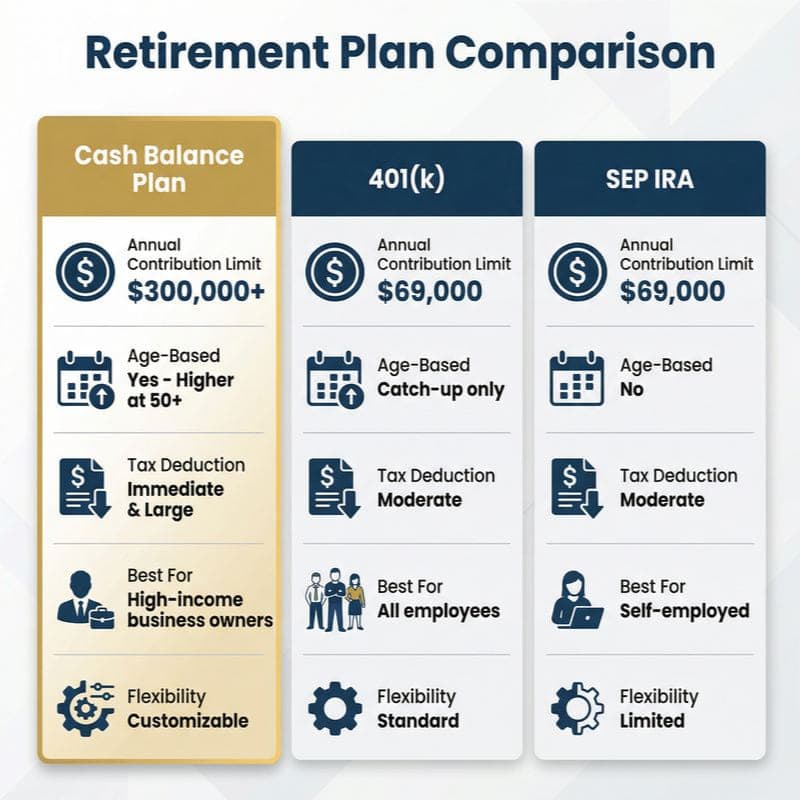

It's a sophisticated, IRS-approved retirement plan that allows high-income earners to make massive, tax-deductible contributions far beyond the limits of a 401(k) or SEP IRA.

Think of it as a 401(k) on steroids. While traditional plans might cap your tax-deductible contributions at around $30,000, a Cash Balance Plan lets you contribute — and deduct — $100,000, $200,000, or even $300,000+ each year.

It's the one structure big enough to turn your biggest liability into your most powerful wealth-building tool.

The Six-Figure Advantages of a Cash Balance Plan

Six-Figure Deductions

Immediately lower your taxable income by contributing hundreds of thousands of dollars annually.

Retroactive Tax Savings

Adopt and fund a plan up to your tax extension deadline to get a “do-over” on last year’s tax bill.

Accelerated Retirement

Super-charge your savings and fill decades of under-funding in just a few peak-earning years.

Flexible Contributions

Match your contributions to your business’s cash flow, dialing them up or down as needed.

Retain Top Talent

Offer a powerful, defined-benefit promise to key employees — a “golden handcuff” without giving up equity.

Advanced Strategy Stacking

Make other tax strategies, like Roth conversions, cheaper and more effective.

Asset & Estate Protection

Shield your wealth from creditors under ERISA and reduce your future estate tax exposure.

How a $249,000 Contribution Saved One Business Owner $92,000 in Taxes — Instantly

A 51-year-old business owner with $440,000 in pass-through profit was facing a massive tax bill.

Instead of accepting it, he adopted a Cash Balance Plan during his tax extension period and made a $249,000 contribution.

The result? An immediate $92,000 reduction in his tax bill. That's money that went directly back into his pocket, not to the IRS.

But the real power is in the long-term wealth shift. Here's a look at the 10-year projection:

Your Advantage: $920,000 saved in taxes, ~$1.0M+ more wealth, tax-free income stream, more for your heirs.

Hypothetical illustration for educational purposes only. Results vary based on individual circumstances.

Will a Cash Balance Plan Work for You? A Quick Checklist

Answer these questions with a simple “Yes” or “No.” If you check three or more boxes, a Cash Balance Plan is likely worth exploring before your tax deadline.

- ✓Will your taxable income exceed $250,000 this year?

- ✓Have you already maxed out your 401(k) or SEP contributions?

- ✓Do you expect high or variable profits over the next 3–5 years?

- ✓Are you between the ages of 40 and 65 and looking to accelerate your retirement savings?

- ✓Would a large deduction this year materially improve your cash flow or reinvestment options?

- ✓Do you want a premium benefit to attract or retain key employees without giving up equity?

- ✓Is reducing your future RMD, IRMAA, or estate-tax exposure important to you?

- ✓Do you file as a Sole Proprietor, S-Corp, C-Corp, or Partnership?

Your Path to Six-Figure Tax Savings in 3 Simple Steps

15-Minute Assessment Call

We’ll analyze your income, entity structure, and goals to provide a personalized contribution estimate and projected tax savings.

Plan Design & Actuarial Modeling

We start with a deep dive into your entire financial picture. We’ll analyze your tax returns, business structures, real estate holdings, retirement accounts, and estate plan to identify every possible opportunity for tax savings.

Fund & Deduct

You fund the plan before your tax deadline and immediately claim your six-figure deduction. Our investment team then manages the assets, turning this year’s tax bill into professionally managed personal wealth.

Common Questions About Cash Balance Plans

I already have a financial advisor. How does this work?+

We can work in two ways. Our Miser Wealth Partners investment division can manage the plan’s assets as part of a fully integrated wealth management strategy. Alternatively, we are happy to coordinate with your existing financial advisor, providing them with the plan’s investment policy statement so they can manage the assets accordingly.

How is this different from a 401(k) or SEP IRA?+

A Cash Balance Plan is a type of defined benefit plan, which allows for much larger, age-based contribution limits than defined contribution plans like 401(k)s. It’s designed to work alongside your existing 401(k) to maximize your tax deductions.

What are the costs to set up and maintain the plan?+

There are setup and annual administration fees, which are typically a small fraction of the tax savings you’ll receive. These fees are also tax-deductible.

What happens if my income goes down?+

The plan has built-in flexibility. You can adjust your contributions within actuarial ranges to match your business’s cash flow, ensuring you stay compliant even in leaner years.

Can I include my spouse?+

Yes, if your spouse is an employee of the business, they can often be included in the plan, potentially doubling the tax-deductible contributions for your household.

How are the funds invested?+

As part of Miser Wealth Partners, the plan’s assets are managed by our in-house investment division. Our team designs a portfolio to target the plan’s required crediting rate while aligning with your long-term wealth goals. This integrated approach ensures seamless management of your tax-deferred assets.

What happens when I retire?+

You have several options. We coordinate with our Miser Wealth Partners legal and investment teams to ensure a seamless transition, whether you choose to roll the funds into an IRA, execute a strategic Roth conversion, or structure tax-efficient distributions as part of your broader estate plan.

Do I have to include all my employees?+

No. Unlike some other retirement plans, Cash Balance Plans can be designed to benefit specific classes of employees, such as owners and key executives, without having to include your entire staff.

Ask Sam about Cash Balance Plans

Ask Sam's AI — it's trained on his methodology and built to help you think through your situation.

This Year’s Tax-Saving Window is Closing.

Every day that passes is a day closer to the tax deadline — the point at which this year’s tax bill becomes permanent. Schedule your no-cost, no-obligation 15-minute assessment today.

Book Your Complimentary Tax AnalysisThis content is for informational purposes only and should not be considered tax, legal, or investment advice. Miser Tax Advisory provides tax services through enrolled agents, legal services through licensed Tennessee attorneys, and investment advisory services through Miser Asset Management, LLC. Every situation is different. Be sure to consult with a qualified tax professional before implementing any strategy discussed herein.